From Soros to Sanctions: The 4 Levers That Rig Emerging Markets – BRICS’ 3 Fixes + 1 Fatal Flaw

Algorithms, derivatives, and debt contracts have replaced the old empires of gunboats and governors. Major financial institutions—hedge funds, investment banks, and multilateral lenders such as the IMF—exert profound control over the economies of developing countries from trading floors in London, New York, and Singapore. This “financial colonization” extracts wealth, dictates policy, and perpetuates dependency, all without a single physical branch or embassy. Through mechanisms such as currency speculation, sovereign debt vulture funds, and conditional lending, these actors can destabilise currencies, inflate import costs, and impose austerity, mirroring colonial tribute systems in a modern guise.

Table of Contents

ToggleThe Invisible Arsenal: Tools of Remote Domination

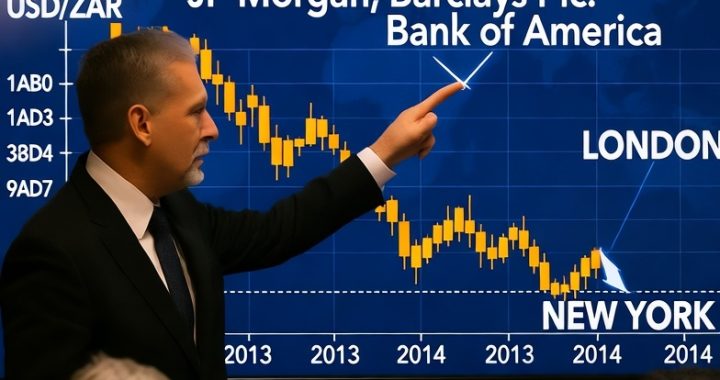

- Currency Manipulation in FX Markets The $7.5 trillion daily foreign exchange (FX) market is dominated by a handful of banks and funds. By executing massive trades remotely, they can swing exchange rates, devaluing local currencies and eroding purchasing power. Emerging market currencies, with thinner liquidity, are especially vulnerable—holiday dumps or benchmark fixes can trigger chaos. Example: In 2017, hedge fund manager Neil Phillips manipulated the USD/ZAR exchange rate from London, selling $725 million to trigger a barrier option and pocket $20 million, thereby spiking rand volatility without ever visiting South Africa.

- Debt Traps and Vulture Funds Developing nations borrow in dollars via international bonds, often from private creditors. When defaults loom, hedge funds buy distressed debt at a low price and demand full repayment plus premiums, holding economies hostage. This “litigation finance” blocks IMF bailouts until concessions are extracted. Example: Sri Lanka’s 2022 default saw hedge funds (holding ~40% of external debt) refuse haircuts, delaying relief and prolonging crisis—despite earning high yields on “risk premiums.” Economists warned that this hard-line stance exemplified the outsized power of private creditors.

- Capital Flows and Sentiment Engineering Sudden inflows fuel booms; abrupt outflows cause busts. Rating agencies (Moody’s, S&P) and funds amplify this by downgrading sovereign debt from afar, raising borrowing costs. IMF loans come with strings: privatize assets, cut subsidies, open markets—effectively outsourcing policy sovereignty.

- Speculative Attacks Hedge funds short currencies en masse, forcing central banks to burn reserves defending pegs. George Soros’s $1 billion profit shorting the Thai baht in 1997 exemplifies this.

|

Mechanism |

Example

Country |

Impact |

Key

Actors |

|

FX

Manipulation |

South

Africa (USD/ZAR) |

Inflated

imports, higher inflation |

Banks

(JPMorgan, Citibank) |

|

Debt

Holdouts |

Sri

Lanka |

Delayed

IMF bailout, prolonged recession |

Hedge

funds |

|

Speculative

Shorting |

Thailand

(1997) |

Baht

devalued 50%, GDP -10.5% |

Soros

Quantum Fund |

|

Conditional

Lending |

Kenya

(2024) |

Tax

hikes sparked Gen Z protests |

IMF |

The 1997 Asian Financial Crisis: The Blueprint

Hedge funds and banks remotely dismantled “Asian Tigers.” Speculators targeted fixed pegs: Thailand’s baht collapsed after $33 billion in futile defence, spreading contagion to Indonesia (-80% rupiah) and South Korea (-50% won)—no invaders were needed; electronic shorts sufficed. GDP plunged in Thailand (-10.5%), sparking riots and regime change. Soros alone profited billions.

South Africa’s Rand Rigging: Cartel from Afar

Between 2007 and 2013, 28 global banks allegedly colluded via chatrooms to manipulate the USD/ZAR exchange rate, thereby widening spreads for their own profit. This weakened the rand, hiking import costs in an economy that is 60% import-dependent. Settlements include Standard Chartered’s R42.7 million fine; the case’s fate hangs on South Africa’s Constitutional Court, which reserved judgment in August 2025. Phillips’s solo 2017 heist reinforced the rand’s fragility.bloomberg.com

Sri Lanka’s Debt Debacle: Vultures Circle

Following the 2022 default on $51 billion in debt, hedge funds demanded no haircuts, stalling IMF aid. Private creditors, who reaped 50% or more of payments via high-yield bonds, profited from the crisis they helped create. One hundred eighty-two economists decried this as a “test case” for global debt norms, with funds’ remote leverage blocking recovery. csis.org

Kenya’s IMF Revolt: Grassroots Pushback

In 2024, IMF-mandated tax hikes in Kenya’s Finance Bill sparked nationwide protests among Gen Z, leading to dilutions. Critics label it “financial imperialism”: $3.5 billion loans tied to austerity, mirroring Zaire’s 1980s playbook of currency devaluation and export focus. brettonwoodsproject.org

The Human Cost and Sovereignty Erosion

Financial colonisation exacerbates inequality: devalued currencies erode the purchasing power of people experiencing poverty through inflation, while elites (often comprador classes) benefit from dollar-denominated assets. Policies shift from domestic welfare to creditor appeasement—subsidies slashed, assets sold. X users echo this: “The IMF traps developing countries in financial chains.”

Yet, it’s not total control. Malaysia’s 1998 capital controls defied IMF orthodoxy and sped recovery. South Africa’s ongoing rand probe signals resistance.

Paths to Liberation:

BRICS Financial Alternatives: Building a Multipolar Economic Order

The BRICS group—originally Brazil, Russia, India, China, and South Africa—has evolved into a coalition of emerging economies seeking greater financial autonomy. Expanded to 11 full members in 2025 (including Egypt, Ethiopia, Iran, the UAE, and Saudi Arabia), BRICS now represents over 45% of the global population and 35% of the world’s GDP. Its financial alternatives aim to address perceived biases in global finance, such as dollar dominance and conditional lending, by promoting local-currency trade, sustainable infrastructure, and de-risked payment systems.

Core Institutions: Parallels to Bretton Woods, But on BRICS Terms

BRICS financial tools mimic yet diverge from those of the IMF and World Bank, emphasising equality among members and a focus on the Global South. Here’s a breakdown:

- New Development Bank (NDB): The “BRICS World Bank”

Established in 2014 and headquartered in Shanghai, the NDB finances infrastructure and sustainable development projects, prioritising emerging markets. Unlike the World Bank, which requires policy conditions, the NDB offers flexible, non-interfering loans in local currencies to mitigate foreign exchange risks.

- Key Features:

- Membership: Original five BRICS nations, with Algeria joining as the first non-BRICS member in 2025. Total subscribed capital: $100 billion (equal shares among founders).

- Funding and Approvals: As of 2025, the NDB has approved $39 billion across 120 projects, generating 2,400 MW of clean energy and avoiding 14.7 million tonnes of CO₂ emissions annually. Recent 2025 approvals include clean energy projects in Brazil ($500M, non-sovereign) and India ($1B, sovereign), as well as transport projects in China.

- Focus Areas: Clean energy (40% of portfolio), transport, water/sanitation, and digital infrastructure. It issues “green bonds” in yuan, rupees, and roubles to diversify from dollar reliance.

Aspect | NDB (BRICS Alternative) | World Bank (Western Model) |

Decision-Making | Equal voting for founders; no veto power | U.S. holds ~16% veto-eligible shares |

Loan Conditions | Minimal; focuses on sustainability | Often includes austerity/fiscal reforms |

Currency Use | Local currencies prioritised | Primarily USD |

2025 Impact | $5B+ in new approvals for Global South | $100B+ globally, but criticised for bias |

The NDB’s Rio de Janeiro Declaration at the July 2025 BRICS Summit emphasised “inclusive governance,” aligning with calls for World Bank reforms.

- Contingent Reserve Arrangement (CRA): The “BRICS IMF”

Launched in 2015, the CRA provides short-term liquidity during balance-of-payments crises, acting as a safety net without the IMF’s structural adjustment programs.

- Key Features:

- Size and Access: $100 billion pool; members can access up to twice their contributions (e.g., China: $41B commitment).

- Usage: Activated twice in 2025—once for South Africa amid rand volatility (linked to the USD/ZAR rigging probes) and once for Ethiopia’s drought response. No conditions imposed, unlike IMF loans.

- Expansion Ties: New members like Saudi Arabia bolster the pool, enhancing crisis response for oil-dependent economies.

This setup echoes the 1997 Asian Financial Crisis, where IMF austerity measures deepened recessions; in contrast, BRICS alternatives prioritise quick, unconditional support.

- Payment and Trade Systems: De-Dollarisation Tools

BRICS is accelerating alternatives to SWIFT (U.S.-controlled) and dollar trade:

- BRICS Pay and Bridge Platform: A blockchain-based system for cross-border settlements in local currencies, piloted in 2025 with Russia-India rupee-rouble trades. Kremlin aide Yury Ushakov described it as a “medium-term ambition” involving digital technology.

- mBridge Initiative: A CBDC (central bank digital currency) platform with China, UAE, and Hong Kong, handling $22 million in pilots by mid-2025. It reduces dollar exposure in 55% of intra-BRICS oil trades.

- No Unified Currency Yet: Despite 2026 speculation post-Kazan Summit, leaders like India’s S. Jaishankar emphasised stability over replacement. The focus remains on gradual de-dollarisation—e.g., 78% of global FX is still USD, but BRICS trade is 60% non-dollar.

Recent Developments: 2025 as a Turning Point

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

BRICS financial momentum surged in 2025 amid U.S. tariff threats and sanctions:

- Expansion and Partnerships: Saudi Arabia’s full membership (July 2025) added $18B to NDB/CRA pools. 13 partners (e.g., Nigeria, Kazakhstan) joined at the 2024 summit, expanding reach.

- SCO Synergies: The Shanghai Cooperation Organisation (SCO) launched its Development Bank in 2025, integrating with NDB for Eurasian projects. This “rewires” finance beyond Bretton Woods.

- De-Dollarisation Push: Intra-BRICS trade hit $500B (majority non-dollar), with China-Russia deals at 90% local currencies. X discussions highlight unity challenges, such as China’s pause on Russian oil following U.S. sanctions, underscoring BRICS as a “loose grouping” rather than an alliance.

At the Rio Summit (July 2025), BRICS+ affirmed bolstering IMF legitimacy while building alternatives, a pragmatic stance amid global tensions.

Cross-Country Patterns: Lessons from Implementation

BRICS alternatives repeat success stories from past crises, adapting to local needs:

- South Africa (Rand Rigging Echoes): NDB’s $1B for water infrastructure (2024-2025) stabilised post-rigging volatility, paralleling CRA’s 2025 liquidity aid—contrasting IMF’s conditional loans in the 1997 Asian Crisis.

- India and Brazil: Local-currency bonds via NDB cut forex risks, mirroring Malaysia’s 1998 capital controls that sped recovery from speculation.

- Iran and Ethiopia: CRA support bypassed U.S. sanctions, akin to Russia’s post-2022 ruble stabilisation—showing how alternatives shield against “financial imperialism.”

- Broader Global South: Algeria’s NDB entry (2025) funds African renewables, echoing Sri Lanka’s 2022 debt woes, where hedge funds delayed IMF relief.

These patterns educate on resilience: BRICS tools prioritise sovereignty, but require domestic reforms for full impact.

Challenges and Criticisms: A Balanced View

While promising, BRICS faces hurdles:

- Internal Divisions: Economic disparities (China’s dominance) and U.S. pressures (e.g., Trump’s 100% tariffs) test unity.

- Scale Limits: NDB’s $39B approvals pale vs. World Bank’s $300B annually; de-dollarisation is gradual (dollar still 78% of FX).

- Geopolitical Risks: Western media critiques BRICS as “anti-dollar bloc,” but leaders like Putin stress complementarity, not confrontation.

Defenders argue these alternatives enhance stability, not disrupt it—e.g., blockchain reduces settlement times from days to seconds.

Conclusion: Toward Inclusive Global Finance

BRICS financial alternatives—such as the NDB, CRA, and payment innovations—offer a multipolar counter to dollar-centric systems, empowering developing economies against remote influences like those seen during the 1997 Asian Crisis or South Africa’s rand scandals. As 2025’s expansions show, they’re evolving from symbolic to substantive, with 2026 potentially launching the BRICS Bridge. For the Global South, this means more equitable access to capital; however, success hinges on unity and practical reforms that can be implemented. Readers: Explore your country’s BRICS ties—tools like NDB projects could reshape local infrastructure. For deeper dives, check recent X threads on de-dollarisation timelines.

About The Author

Lungi Nkosi

Hi, I’m Lungi, the writer and researcher behind Political Nexus. I started this blog because I believe politics and history aren’t just distant, academic subjects — they shape how we live, how we understand the world, and how we imagine the future.

I’m not here to lecture; I’m here to ask questions, share insights, and spark conversations. Whether it’s unpacking a breaking news story, looking back at a key moment in history, or analyzing the choices of today’s leaders, I aim to keep things clear, thoughtful, and engaging.

My interest in politics and history comes from a lifelong curiosity about power — who holds it, how it’s used, and how ordinary people are affected by it. Over the years, I’ve seen how narratives are built, how facts are bent to fit agendas, and how history is used as both a weapon and a guide. That’s why Political Nexus is more than a blog — it’s a space for reflection, inquiry, and conversation.

I write about:

Politics: current events, government decisions, and global trends that affect South Africa and beyond.

History: how past events continue to echo in today’s politics and society.

Media & Narratives: questioning how stories are told, what gets left out, and why.

When I’m not writing, you can usually find me [behind the computer creating stories to tell, exploring books on history and philosophy, debating ideas over coffee with friends, or experimenting with new projects.

At the heart of it, I see myself as a storyteller — one who isn’t afraid to challenge easy answers, ask uncomfortable questions, and look deeper than the surface. My hope is that readers like you walk away from each article not just more informed, but more curious.

So, welcome to Political Nexus. Let’s explore, question, and learn together.

Part 2.1: The Rand Rigging Saga

Part 2.1: The Rand Rigging Saga  Part 2: London Typed 3 Words → Your Bread Jumped 15 %. The $10 Billion Forex Cartel

Part 2: London Typed 3 Words → Your Bread Jumped 15 %. The $10 Billion Forex Cartel  Part 1: Why Banks Manipulate Currencies

Part 1: Why Banks Manipulate Currencies  Rights Without Capacity: Is South Africa Building an Illusion of Delivery?

Rights Without Capacity: Is South Africa Building an Illusion of Delivery?  Who Funds Court Rulings?

Who Funds Court Rulings?  Media, Rulings & Policy Flow: How Courts Quietly Shape South African Governance

Media, Rulings & Policy Flow: How Courts Quietly Shape South African Governance  Framing the Nation: How Media Narratives Shape Political Reality in South Africa

Framing the Nation: How Media Narratives Shape Political Reality in South Africa